Liza Mirandilla, an employee in a fruits and vegetables store in New Lucena City Public Market is nearing her retirement age. Despite working for 33 years, Liza will not receive a pension nor does she and her husband have any retirement plan or health insurance. Her family relies on ‘five-six’ money lending—a now illegal informal type of money lending service with 20% interest—for their daily spendings and to fund the education of their 6 children.

“Kaya naman ako nangungutang sa ‘five-six’ kasi may pinag-aaral ako na mga anak—tatlo pa yung nasa kolehiyo. Parang kapag mangungutang ako ay kulang talaga sa pinansyal. Kasi hindi naman sumasapat ang sweldo ng aking mister dahil sa mahal na mga bilihin,” explaining why she choose to rely on ‘five-six’ money lending despite the high-interest.

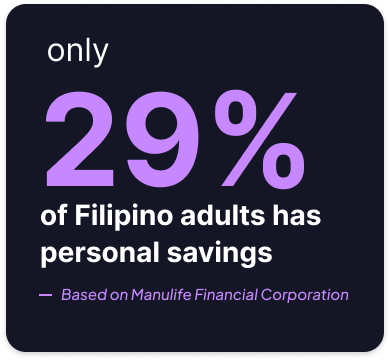

Just like her, around 80% of Filipino senior citizens have no mandatory pension coverage, primarily due to the large informal workforce and limited access to social security. And only around 29% of Filipinos have any form of personal savings—making us among the lowest in Southeast Asia. These figures are generally contributed by the lack of financial literacy, cultural attitudes, deprioritization of long-term financial planning and other financial constraints.

Liza once ran a successful pares shop. On a good day, she earned over a thousand pesos, making it a sustainable and profitable venture for their family. However, the demands of running the business alone took a toll on her health.

“Kumikita naman ako ng higit sa 1k doon sa mami-pares, kaya lang sumasama talaga ang aking pakiramdam at nagkakasakit ako. Baka mas kulang pa nga ang pampagamot,” she shared, noting that her earnings would likely not cover medical expenses if she continued working herself to exhaustion.

Had Liza had access to business-specific banking services, she might have been able to secure the capital to hire extra workers for her pares shop. This support could have prevented her from having to quit out of fear of getting sick from working alone to sustain her business.

Had Liza had access to formal bank loans, such as BPI’s Ka-Negosyo Loan, she might have been able to sustain her business with extra help and avoid health risks from overwork. BPI’s Ka-Negosyo Loans cater to small and medium enterprises, offering options to fund business operations, property acquisition, or capital expansion.

This program allows entrepreneurs like Liza to choose between a secured or unsecured loan depending on their capacity, often with favorable terms like fixed-rate interest and the flexibility to use collateral only if necessary. By providing more stability in funding, Ka-Negosyo Loans could have helped Liza invest in hiring additional staff, easing her workload and enabling her to keep her store open longer, without risking her health.

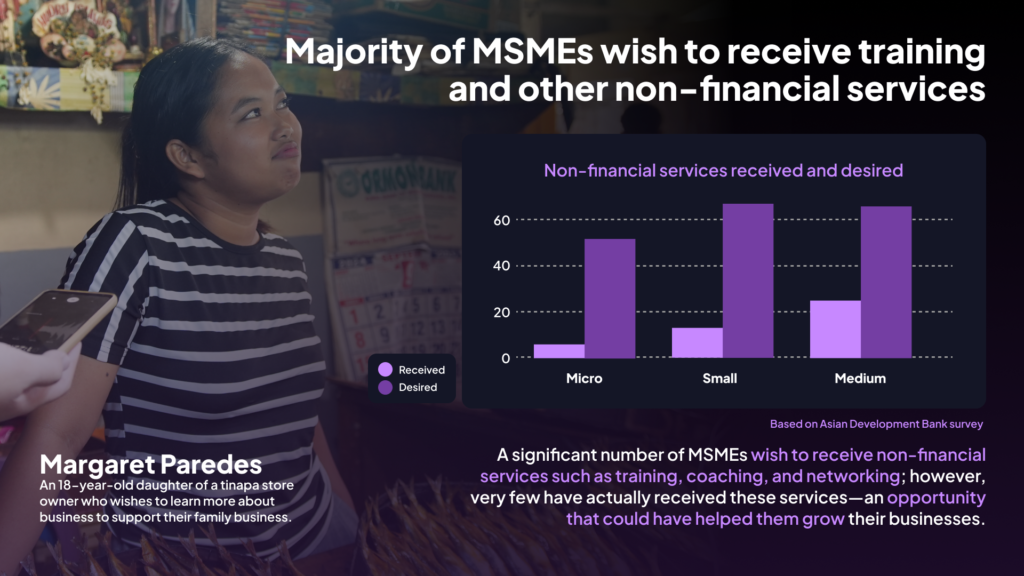

Furthermore, with proper training in business management, Liza could have planned her pares venture more effectively, anticipating and mitigating the risks associated with running a small enterprise. Unfortunately, many MSMEs lack access to essential training and non-financial support services, often leaving entrepreneurs to dive into business ventures without the foundational knowledge necessary for sustainable growth and success.

Liza Mirandilla’s story highlights the harsh reality faced by many Filipinos in the informal sector, where limited access to financial resources and a lack of safety nets like pensions and insurance leave them vulnerable. Her reliance on high-interest loans underscores the necessity for better financial inclusion and access to formal credit systems. With tools like BPI’s Ka-Negosyo Loans, small business owners could empower themselves to grow sustainably, reduce their dependence on informal lending, and safeguard their health and financial future. As a society, it’s time we invest in financial literacy, expand access to responsible lending, and create policies that support small entrepreneurs. The government, financial institutions, and businesses must work together to build an ecosystem that helps people like Liza thrive, ensuring a secure future for all.