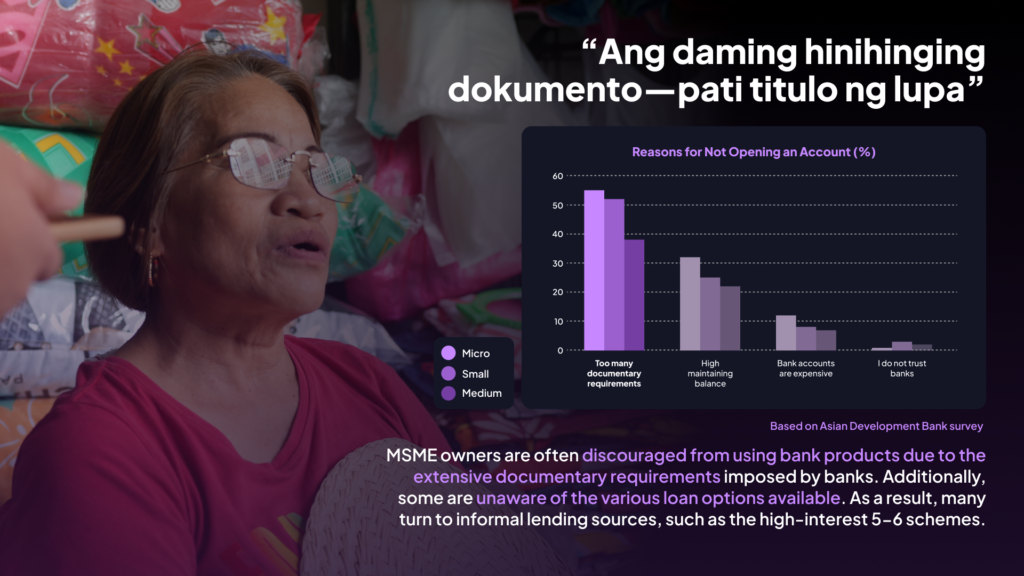

Felisa Edian is a door rug vendor who sells her products on the sidewalk without a legal permit. Like many others in the informal economy, she avoids taking loans from banks, fearing she would need to pledge the title of her land as collateral. “Ang dami nilang hinihinging dokumento at kapag umutang ka doon, may prendang mga titulo, ganun. Nakakatakot umutang,” she explains. This discouragement is common among many Filipinos; in fact, over 50% of micro enterprises are unbanked, citing extensive documentary requirements as the primary barrier.

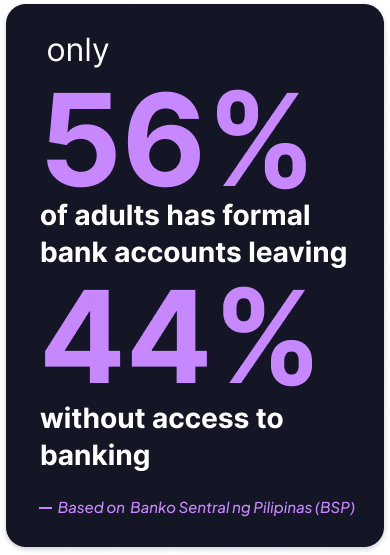

The stigma around formal bank loans among small vendors like Felisa is part of a larger pattern of financial exclusion in the Philippines. According to the Bangko Sentral ng Pilipinas (BSP), as of 2021, around 56% of adults had a formal bank account, leaving nearly half of the population without access to banking. This limited engagement with formal credit channels leads many to rely on informal lending, such as the “five-six” system, where exorbitant interest rates often trap borrowers in cycles of debt.

The stigma around formal bank loans among small vendors like Felisa is part of a larger pattern of financial exclusion in the Philippines. According to the Bangko Sentral ng Pilipinas (BSP), as of 2021, around 56% of adults had a formal bank account, leaving nearly half of the population without access to banking. This limited engagement with formal credit channels leads many to rely on informal lending, such as the “five-six” system, where exorbitant interest rates often trap borrowers in cycles of debt.

Collateral requirements are indeed a deterrent: only about 4% of Filipinos with outstanding loans borrow from banks, while most turn to informal sources. The BSP’s 2021 Financial Inclusion Survey highlights that lack of collateral, alongside a lack of trust in financial institutions and limited awareness of banking services, are major reasons Filipinos avoid formal credit.

Felisa’s experience reflects the hardships of informal vendors in the Philippines, who often face harassment from authorities due to their lack of legal vending stalls. As a result, she has been chased by government employees, and at times, her products were seized, requiring her to pay fines to retrieve them.

She shared, “Dati hinahabol kami ng mga traffic enforcer d’yan at ayaw kaming patayuin nga d’yan sa may bangketa. Tinubos ko noon ng P200 noong nakunan ako ng bedsheet tapos pinuntahan ko doon sa opisina nila.” This predicament continued until a generous establishment owner allowed her to sell her rugs in their garage, offering a temporary solution to her struggle.

Felisa also recounted that she previously rented a stall within the market but had to give it up due to the exorbitant rental fees. “Isipin mo pa ang pagbabayad sa pwesto, magkano ang pinakamababang pwesto? nasa 30,000 to 40,000 pesos, kung kukuha pa ako, sakit lang sa ulo. Buti kung ang makukuha mong pwesto ay malakas, kung wala masyadong mamimili edi lugi ka,” she explained.

However, lately, as digital shops have emerged, Liza explains that her sales have been decreasing. Although she wants to try selling online, she admits that she lacks sufficient knowledge and fears she might end up getting scammed out of her products. Many MSMEs in the older age group echo the same sentiment.

For many informal vendors like Felisa, the cost of legal vending spaces remains prohibitively high, often leading them into vulnerable positions where they face fines and constant risk of eviction. BPI’s Ka-Negosyo Loan could provide an essential lifeline by offering affordable financial support tailored for small entrepreneurs. With flexible repayment terms and competitive interest rates, this loan could help Felisa cover the cost of renting a legal stall, giving her a more stable and secure business setup.

Additionally, BPI’s Small Enterprise Acceleration Lab can provide Felisa with the tools she needs to strengthen her business, offering training in crucial areas like cash flow management, budgeting, and long-term business planning. This program aims to equip small business owners with the financial literacy necessary to navigate the complexities of managing a business and making informed financial decisions. By participating in these workshops, Felisa can gain the knowledge needed to not only access funding but also strategically grow her business and ensure its sustainability. Such a holistic approach, combining financial education with practical support, will empower her to transition away from the cycle of fines and instability, setting a strong foundation for her business and her family’s future.